Brand Valuation

Brand value is the determination of the independent value of the brand in the market, apart from the physical assets of the business. Brand valuation, which enables the determination of financial superiority over other brands, has become an economic necessity today. The reason for this is;

Brand valuation and awareness reports are also important factors taken into account when calculating the value of the company in brand valuation acquisitions and mergers.

In addition, when there is a situation such as share transfer or sharing in the company, the brand will be shared along with the physical assets.

In trademark transfer transactions, the correct determination of the value of the trademark is of great importance for the buyer and seller.

The trademark valuation report is one of the most important references to be submitted to the court in case of litigation in the same sector or in related fields of activity in case of loss of rights arising from similarity or imitation.

Trademark valuation is very important for determining the price to be demanded in cases where trademark rights are made available to another business for a period of time (licensing, dealer & franchise).

The trademark valuation report to be submitted to the relevant bank in loan purchases has a positive impact on the loan process.

If a well-known trademark application is planned, one of the criteria for a well-known trademark is the financial strength of the trademark. At this point, brand valuation has a positive contribution to the process.

International Valuation Standards

In accordance with paragraph 1 of Article 30 of International Valuation Standards 104 (“IAS 104”);

“Market value is the estimated amount that would be required to settle the exchange of an asset or liability between a willing seller and a willing buyer, as a result of appropriate marketing activities, in an arm’s length transaction between knowledgeable, prudent and uncoerced parties.”

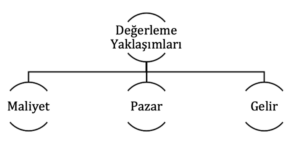

According to paragraph 1 of Article 10 of IAS 105 Valuation Approaches and Methods, there are three main

There is a valuation approach.

Valuation Approaches

In the cost approach, the indicative value is determined by calculating the current replacement cost or reproduction cost of an asset and deducting all allowances for physical deterioration and other forms of depreciation.

The market approach is the approach in which the indicative value is determined by comparing the asset with identical or comparable (similar) assets for which price information is available.

The income approach allows the indicative value to be determined by converting future cash flows into a single current value. Under the income approach, the value of the asset is determined based on the present value of the revenues, cash flows or cost savings generated by the asset (IAS 105, item 40 paragraph 1). Although there are many ways of applying the income approach, the methods within the income approach are actually based on discounting future cash amounts to present value. These are variations of the Discounted Cash Flow (DCF) method.

Gizpatent Makes a Difference

As Giz Patent, we prefer the income approach model as it provides more realistic data, which is the most preferred of the three basic valuation approaches.

The cost approach is not preferred due to the uncertainties about which costs will be added to the brand value and the fact that it is very difficult to decide how the expenditures made indirectly to support the brand will be added to the brand value.

The market approach is not preferred due to the difficulty of comparing brands with each other as they are different assets, and the inability to find the market price of a similar brand as brands are not assets that are constantly traded.